Date

March 10, 2026

5 min read

The Scrutiny Shift: Why Higher-Frequency Valuations Create a Math Problem Most Firms Can’t Solve

Private credit firms aren’t being asked to do something new. They’re being asked to do the same work but more often, with more scrutiny, and with less tolerance for reconstruction. Quarterly valuation cycles are giving way to monthly, weekly, and in some cases daily marks. Not because regulators suddenly changed the rules, but because capital did. Evergreen vehicles, semi-liquid structures, NAV financing, and retail inflows all demand tighter cadence and clearer answers. This shift exposes a simple reality: This is not regulatory panic. It’s math. And the math doesn’t work unless the operating model changes.

More Frequency Doesn’t Mean More Speed: It Means More Work

At first glance, higher-frequency valuation sounds like a speed problem. In reality, it’s a volume problem. Every valuation cycle requires updated market data, refreshed assumptions, documented inputs, versioned outputs, and the ability to explain why something moved, not just that it moved. By increasing frequency, you are not only shortening timelines, but you are multiplying the number of valuation events that must be executed, stored, and later defended. Let’s make the math explicit.

The Math Problem (Why This Breaks So Quickly)

Assume a conservative private credit portfolio:

- 45 credit positions

- ~2 hours per asset per valuation cycle (data intake, refresh, review, documentation) // ~1 hour per asset per valuation cycle for weekly or daily

Now look at cadence:

| Valuation Frequency | Cycles per Year | Total Asset Valuations | Approx. Hours / Year |

| Quarterly | 4 | 180 | ~360 hours |

| Monthly | 12 | 540 | ~1,080 hours |

| Weekly | 52 | 2,340 | ~2,340 hours (1 hr/val) |

| Daily (250 days) | 250 | 11,250 | ~11,250 hours (1 hr/val) |

A quarterly process that “works fine” becomes mathematically impossible at weekly or daily frequency… unless the nature of the work fundamentally changes. No valuation team is scaling headcount 10x to 60x. And even if they could, the risk profile would be unacceptable.

Scrutiny Is Applied Later: That’s the Catch

The most dangerous misunderstanding firms make is assuming scrutiny increases at the same time as frequency. Scrutiny shows up later:

- Auditors asking about a mark from 18 months ago

- IC or risk committees revisiting assumptions after volatility

- Banks and NAV lenders reconciling valuation logic across reporting periods

- LPs comparing disclosures across funds and vehicles

And audits don’t look back five days. They look back five years. As valuation events multiply, so does the surface area for questions. The issue becomes whether you can reconstruct how you arrived at a number, precisely, months or years from now.

Where the Process Actually Breaks: Data Lineage

Firms often assume the breaking point is analyst capacity. That’s visible, but it’s not the root cause – the real failure point is data lineage.

When frequency increases, 1) inputs change more often 2) assumptions evolve continuously 3) versions multiply and 4) dependencies compound.

Without a governed system of record, 1) you lose the ability to trace inputs to outcomes, 2) you rely on memory, emails, and spreadsheets to explain decisions and 3) each answer becomes a bespoke reconstruction exercise.

You may still be able to produce a valuation but defending it later is where things fall apart.

What Firms Try First (And Why It Fails)

Before turning to technology, most firms attempt predictable fixes:

More spreadsheets

Templates proliferate. Version control collapses.

More people

Analysts spend more time copying data than analyzing it.

Offshore teams

Labor shifts, but the process remains fragile.

Fully subcontract to a third party

Labor shifts and opinion transfers, but at higher cost — and with loss of control over process and data.

Heroics

Smart people working late nights to “get it done”—until scrutiny spikes.

These approaches may help you survive the next cycle. They do nothing to prepare you for the next 50. Spreadsheets don’t fail in calm markets. They fail when leadership is personally accountable for quickly explaining outcomes.

Technology Isn’t About Speed: It’s About Changing the Work

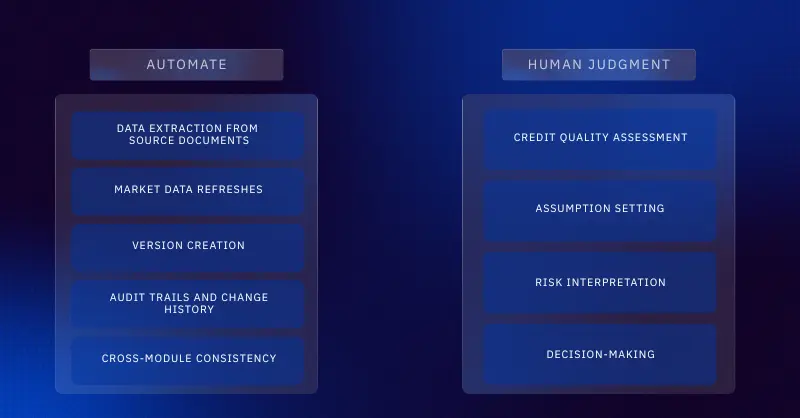

Higher-frequency valuation doesn’t require humans to work faster. It requires humans to work differently. The only scalable model separates 1) what must be automated and 2) what must remain judgement.

Technology becomes a force multiplier, not a replacement. It allows the same team to operate at higher frequency without sacrificing defensibility.

Why This Favors Purpose-Built Platforms

This is where generic tooling breaks down. Spreadsheets can calculate values. They cannot:

- Store every input across thousands of valuation events

- Maintain clean lineage between documents, assumptions, and outcomes

- Provide instant historical explainability under pressure

Purpose-built platforms are designed for exactly this problem. Firms like Hamilton Lane and Blackstone have already recognized that higher frequency without governance creates more risk, not less. Platforms like 73 Strings exist because the market moved first and the operating model has to catch up.

The Real Question C-Suite Leaders Should Be Asking

Not: Can we value more often?

But: Can we defend every valuation event we create, at scale, over time?

Because once you move to weekly or daily cadence, you can’t selectively apply rigor. Every mark becomes part of your permanent record. Speed without defensibility is a liability.

The Takeaway

Higher-frequency valuation is a consequence of how private credit is evolving.

The math is unavoidable: more cycles, same teams, higher scrutiny, and longer lookbacks

Firms that treat this as a tooling upgrade will struggle. Firms that treat it as an operating-model transformation will pull ahead. If you’re moving toward weekly or daily valuation, the question isn’t whether you need technology. It’s whether your current process can survive the math.

Want to see how leading firms move to higher-frequency valuations without adding headcount? That’s where the real conversation starts.